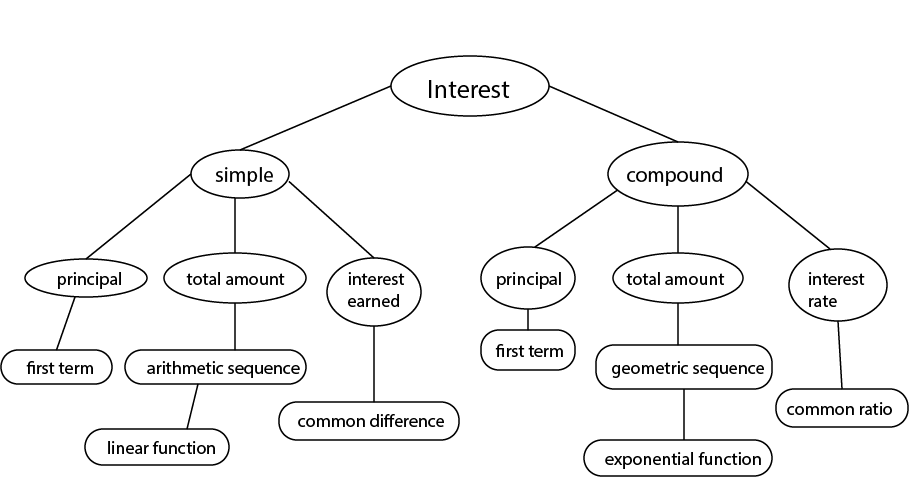

All Solutions

Section 8-2: Compound Interest: Future Value

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

Also remember the following terms.

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

defarraystretch{2}%

begin{tabular}{|l|l|l|}

hline

mode & $i=dfrac{r}{n}$ & $m=ncdot t$ \ hline

semi-annual & $frac{1}{2}cdot 0.054=0.027$ & $5cdot 2=10$ \ hline

monthly & $frac{1}{12}cdot 0.036=0.003$ & $3cdot 12=36$ \ hline

quarterly & $frac{1}{4}cdot 0.029=0.00725$ & $7cdot 4=28$ \ hline

daily & $frac{1}{52}cdot 0.026=0.0005$ & $frac{10}{12}cdot 52=43frac{1}{3}$ \ hline

end{tabular}

end{table}

defarraystretch{2}%

begin{tabular}{|l|l|l|}

hline

mode & $Interest;Rate;per;Compounding;Period$ & $Compounding;Period$ \ hline

semi-annual & $frac{1}{2}cdot 0.054=0.027$ & $5cdot 2=10$ \ hline

monthly & $frac{1}{12}cdot 0.036=0.003$ & $3cdot 12=36$ \ hline

quarterly & $frac{1}{4}cdot 0.029=0.00725$ & $7cdot 4=28$ \ hline

daily & $frac{1}{52}cdot 0.026=0.0005$ & $frac{10}{12}cdot 52=43frac{1}{3}$ \ hline

end{tabular}

end{table}

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

Also remember the following terms.

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

a.) We shall calculate the accumulated amount for the first 5 years

Since this is compound interest, the common ratio between consecutive compounding period is $left(1+iright)$. In this case, $i=7.2%=0.072$ and compounded annually

1st year: $A(1)=10,000(1.072)=$10;720$

2nd year: $A(2)=10,720(1.072)=$11;491.84$

3rd year: $A(3)=11,491.84(1.072)=$12;319.25$

4th year: $A(4)=12;319.25(1.072)=$13;206.24$

5th year: $A(5)=13;206.24(1.072)=$14;157.09$

The amount after $k$ years,

$A(k)=10;000(1.072)^k$

Since this is compound interest, the common ratio between consecutive compounding period is $(1+i)$. In this case, $i=1.9%=0.019$ and compounded semi-annually.

1st half-year: $A(1)=10,000(1.019)=$10;190$

2nd half year: $A(2)=10,190(1.019)=$10;383.61$

3rd half year: $A(3)=10,383.61(1.019)=$10;580.90$

4th half year: $A(4)=10;580.90(1.019)=$10;781.94$

5th half year: $A(5)=10;781.94(1.019)=$10;986.80$

The amount after $k$ half-years,

$A(k)=10;000(1.019)^k$

Since this is compound interest, the common ratio between consecutive compounding period is $(1+i)$. In this case, $i=1.7%=0.017$ and compounded semi-annually.

1st quarter: $A(1)=10,000(1.017)=$10;170$

2nd quarter: $A(2)=10;170(1.017)=$10;342.89$

3rd quarter: $A(3)=10;342.89(1.017)=$10;518.72$

4th quarter: $A(4)=10;518.72(1.017)=$10;697.54$

5th quarter: $A(5)=10;697.54(1.017)=$10;879.40$

The amount after $k$ quarters,

$A(k)=10;000(1.017)^k$

Since this is compound interest, the common ratio between consecutive compounding period is $(1+i)$. In this case, $i=0.9%=0.009$ and compounded semi-annually.

1st month: $A(1)=10,000(1.009)=$10;090$

2nd month: $A(2)=10;090(1.009)=$10;180.81$

3rd month: $A(3)=10;180.81(1.009)=$10;272.44$

4th month: $A(4)=10;272.44(1.009)=$10;364.89$

5th month: $A(5)=10;364.89(1.009)=$10;458.17$

The amount after $k$ months,

$A(k)=10;000(1.009)^k$

b.) $A(k)=10;000(1.019)^k$

c.) $A(k)=10;000(1.017)^k$

d.) $A(k)=10;000(1.009)^k$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

Also remember the following terms.

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

In this case,

$A(t)=P(1+i)^m$

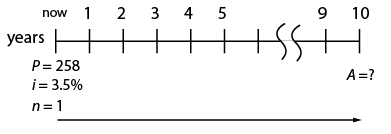

a.) In this case,

$P=$258$

$r=3.5%=0.035$

$n=1$ (annually)

$A=258(1+0.035)^{10}=$363.93$

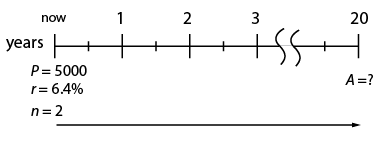

$P=$5000$

$r=6.4%=0.064$

$n=2$ (semi-annually)

$t=10;years$

$A=5000left(1+dfrac{0.064}{2}right)^{2cdot 10}=$363.93$

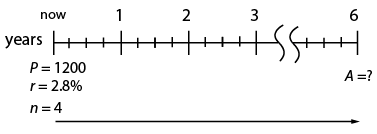

$P=$12000$

$r=2.8%=0.028$

$n=4$ (quarterly)

$t=6;$ years

$A=1200left(1+dfrac{0.028}{4}right)^{4cdot 6}=$1418.69$

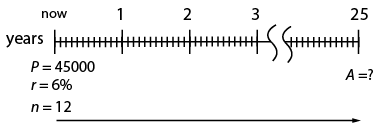

$P=$45000$

$r=6%=0.06$

$n=12$ (monthly)

$t=25$ years

$A=45000left(1+dfrac{0.06}{12}right)^{12cdot (25)}=$200923.64$

b.) $$17;626.17$

c.) $$1418.69$

d.) $$200;923.64$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

Also remember the following terms.

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A(t)-P=P[(1+i)^m-1]

$$

a.) We are given with

$P=4000$

$i=0.03$

$m=4$

Using the formula above,

$A=P(1+i)^m=4000(1+0.03)^4=$4502$

$$

I=A-P=4502.04-4000=$502.04

$$

$P=7500$

$i=0.005$

$m=72$

Using the formula above,

$A=P(1+i)^m=7500(1+0.005)^{72}=$10;740.33$

$$

I=A-P=10740.33-7500=$3240.33

$$

$P=15000$

$i=0.006$

$m=20$

Using the formula above,

$A=P(1+i)^m=15000(1+0.006)^{20}=$16;906.39$

$$

I=A-P=16906.39-15000=$1906.39

$$

$P=28200$

$i=0.0275$

$m=20$

Using the formula above,

$A=P(1+i)^m=15000(1+0.006)^{20}=$48;516.08$

$$

I=A-P=48;516.08-28;200=$20;316.08

$$

$P=850$

$i=0.0001$

$m=365$

Using the formula above,

$A=P(1+i)^m=850(1+0.0001)^{365}=$881.60$

$$

I=A-P=881.60-850=$31.60

$$

$P=2225$

$i=0.001$

$m=47$

Using the formula above,

$A=P(1+i)^m=2225(1+0.001)^{47}=$2332.02$

$$

I=A-P=2332.02-2225=$107.02

$$

b.) $A=$10;740.33$ ; $I=$3240.33$

c.) $A=$16;906.39$ ; $I=$1906.39$

d.) $A=$48;516.08$ ; $I=$20;316.08$

e.) $A=$881.60$ ; $I=$31.60$

d.) $A=$2332.02$ ; $I=$107.02$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

a.) Remember that ratio of $A$ between consecutive compounding is $left(1+dfrac{r}{n}right)$. For annual compounding, $n=1$, so this ratio becomes $(1+r)$

$$

dfrac{4404.404240}{4240}=1+rimplies r=dfrac{4404.404240}{4240}-1=0.06=boxed{bold{6%}}

$$

$$

A=Pleft(1+dfrac{0.06}{1}right)^{1(1)}implies P=dfrac{4240}{1+0.06}=boxed{bold{$4000}}

$$

b.) $$4,000$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

Here we are given with $A=25;000$, $r=0.07$, $P=10;000$, and monthly compounding (n=12).

We shall find how long will it take to reach $$25;000$.

Using the formula

$A=Pleft(1+dfrac{r}{n}right)^m$

$A=Pleft(1+dfrac{0.07}{12}right)^{m}$

$25,000=10,000left(1+dfrac{0.07}{12}right)^mimplies 2.5=left(1+dfrac{0.07}{12}right)^m$

We shall try several values of $m$

if $m=156implies left(1+dfrac{0.07}{12}right)^{156}=2.4778$

if $m=157implies left(1+dfrac{0.07}{12}right)^{157}=2.4922$

if $m=158implies left(1+dfrac{0.07}{12}right)^{158}=2.5068$

Thus, the account value will be at least $25,000$ at the 158$^{th}$ compounding.

Since compounding is done every month, this is also $boxed{bold{158; months}}$.

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We shall find which one is a cheaper option for $P=15,000$

Option 1:

$r=0.1$

$n=4$ (quarterly)

$t=10;text{years}$

Option 2:

for first 5 years:

$r=0.12$

$n=4$

$t=5;text{years}$

for next 5 years:

$r=0.06$

$n=4$

$t=5;text{years}$

$A=15,000cdot left( 1+dfrac{0.1}{4}right)^{4(10)}=underline{$40,275.96}$

Option 2:

$A_1=15,000cdot left( 1+dfrac{0.12}{4}right)^{4(5)}=$27,091.67$

$A_2=27,091.67cdot left(1+dfrac{0.06}{4}right)^{4(5)}=$36;488.55$

Total = $$27,091.67+$36,488.55=underline{$36,488.55} ;;checkmark$

Therefore, Option 2 is cheaper by $40275.96-36488.55=$3787.41$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

By inspection, you can see that in the formula

$A(n)=5000times (1.0075)^{12n}$

$P=$5000$

$i=0.0075$

$n=12$ (monthly compounding)

$r=icdot n=0.0075cdot 12=0.09=9%$ per annum

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We shall evaluate which payment plan is cheaper for $P=949.99$

Plan A: simple interest, $r=0.10$ for 2 years

$A=P(1+rt)$

$A_A=949.99(1+0.1cdot 2)=boxed{$1399.99}$

Plan B: compound interest, $i=0.0125$, $m=8$

$A=P(1+i)^m$

$A_B=949.99(1+0.0125)^8=boxed{$1049.25};;checkmark$

Plan B is cheaper by $1399.99-1049.25=$290.64$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

In this case, we are given with $P=1000$, $i=5%=0.05$, and $m=7$.

We can determine the future value after 7 compounding using this formula:

$A=P(1+i)^m$

$A=1000(1+0.05)^7=boxed{bold{$1407.10}}$

$1407.10

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

In this case, we are given with

for first 3 years: $P=9000$ ; $r=10%=0.1$ ; $n=4$

for next 2 years: $r=9%=0.09$ ; $n=2$

Using the formula, the amount after 3 years is

$A_1=Pleft(1+dfrac{r}{n}right)^{nt}=9000left(1+dfrac{0.1}{4}right)^{4cdot 3}=9000left(1+dfrac{0.1}{4}right)^{4(3)}=$12;104.00$

The amount after 3 years will be the principal for the next two years

$A_2=12104.00left(1+dfrac{0.09}{2}right)^{2(2)}=$14;434.24$

The amount after 5 years is $boxed{bold{$14;434.24}}$

$14;434.24

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

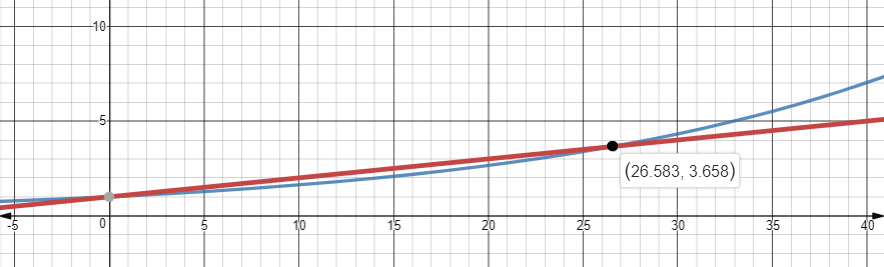

We need to how many years will a simple interest with annual rate of $10%$ would have equal value with a compound interest with $5%$ annually.

$Pleft(1+rtright)=Pcdot (1+r)^{t}$

$1+0.05t=(1+0.05)^{t}$

This equation is difficult to solve analytically, so we will solve it graphically.

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We have to cases:

(a) $$5000$ at $5%$ compounded annually

(b) $$3000$ at $7%$ compounded annually

$5000cdot (1.05)^t=3000(1.07)^t$

$left(dfrac{1.07}{1.05}right)^t=dfrac{5000}{3000}=1.66667$

We shall find value $t$ by taking several values of $t$

$t=26implies left(dfrac{1.07}{1.05}right)^{26}approx 1.6333$

$t=27implies left(dfrac{1.07}{1.05}right)^{27}approx 1.6644$

$t=28implies left(dfrac{1.07}{1.05}right)^{28}approx 1.6961$

Thus, the two cases would have equivalent value at around $boxed{bold{ 27 years}}$.

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We will calculate the future worth of $P=$1$ after 1 year to compare which investment plan is more profitable.

Case 1: $6.5%$ quarterly

$A=1cdotleft(1+dfrac{0.065}{4}right)^4approx 1.066602$

Case 2: $6.55%$ semi-annually

$A=1cdot left(1+dfrac{0.0655}{2}right)^2approx 1.066572$

Case 3: $6.45%$ monthly

$A=1cdot left(1+dfrac{0.0645}{2}right)^{12}approx 1.066441$

Case 4: $6.6%$ annually

$A=1cdot left(1+dfrac{0.066}{1}right)^{1}=1.066$

Therefore, $6.5%$ compounded quarterly is more profitable.

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We shall find the amount on July 1, 2001:

$P=2000$ ; $i=0.5%=0.005$, $m=60$

$A_1=2000(1+0.005)^{60}=$2697.70$

The new principal for the next 26 compounding is $$2697.70$

$P=2697.70$ , $i=0.02$, $m=26$

$A_2=2697.70(1+0.02)^{26}=$4514.48$

Therefore, the account value on the first day of 2008 is $boxed{bold{$4,514.38}}$

$4,514.38

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

We’re given $P=4000$, $r=4%=0.04$, compounded quarterly (n=4).

The amount after 1 year

$A=Pleft(1+dfrac{r}{n}right)^{nt}=4000left(1+dfrac{0.04}{4}right)^{4(1)}=$4162.42$

For the second year $r=4.2%=0.042$

$A=4162.42left(1+dfrac{0.042}{4}right)^{4(1)}=$4340.01$

For the third year: $r=4.4%=0.044$

$A=4340.01left(1+dfrac{0.044}{4}right)^{4(1)}=$4534.14$

The amount after third year is $boxed{bold{$4534.14}}$

$4534.14

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

For the first five years, $P=500$, $r=4.8%=0.048$, $n=12$ (monthly compoundly)

$A_1=500left(1+dfrac{0.048}{12}right)^{12(5)}=$635.32$

On her 5th birthday, she received another $$500$, so the amount on her $10^{th}$ birthday is

$A_2=(635.32+500)left(1+dfrac{0.048}{12}right)^{12(5)}=$1442.58$

On her 10th birthday, she received another $$500$, so the amount on her $15^{th}$ birthday is

$A_3=(1442.58+500)left(1+dfrac{0.048}{12}right)^{12(5)}=$2468.32$

On her 15th birthday, she received another $$500$, so the amount on her $18^{th}$ birthday is

$A_4=(2468.32+500)left(1+dfrac{0.048}{12}right)^{12(3)}=$3427.08$

The account value on her 18th birthday is $boxed{bold{$3427.08}}$.

$3427.08

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

With semi-annual compounding, there will be $20$ compounding period within 10 years. Every period, Anita adds $$500$ from an initial investment $P=$500$, $n=2$, $r=6.8%=0.068$, $i=frac{r}{n}=frac{0.068}{2}=0.034$ and $t=10;$ years.

The principal $$500$ will be compounded $10times 2=20$ times, thus

$A_0=500(1+0.034)^{20}$

The first added $$500$ will be compounded 19 times,

$A_1=500(1+0.034)^{19}$

The second added $$500$ will be compounded 18 times

$A_2=500(1+0.034)^{18}$

Thus, the amount due to the $k^{th}$ investment is

$A_k=500(1+0.034)^{20-k}$

The total investment at 20th compounding is then a geometric series with

$t_1=500(1.034)^{19}=943.76$

$r=dfrac{500(1.034)^{19}}{500(1.034)^{20}}=dfrac{1}{1.034}$

$S_{20}=t_1cdot dfrac{r^n-1}{r-1}=943.76cdot dfrac{(1/1.034)^{20}-1}{(1/1.034)-1}=13995.48$

Therefore, after 10 years, the account value would be $boxed{bold{$13,995.48}}$.

$$

A=Pcdot dfrac{(1+i)^m-1}{i}=500cdot dfrac{(1+0.034)^{20}-1}{0.034}=$13995.48

$$

$13,995.48

$$

$A(t)=Pleft(1+dfrac{r}{n}right)^{nt}$

where

$A(t)$ = future value of investment or debt after $t$ years

$P$ = principal or initial deposit or debt

$r$ = annual interest rate

$n$ = number of compounding per year ($n=1$ for annually, $n=2$ for semi-annually, $n=4$ for quarterly, $n=12$ for monthly)

$t$ = number of years that the money is invested or borrowed

$bold{Useful;Definitions}$

Interest Rate per Compounding Period: $i=dfrac{r}{n}$

Number of Compounding Periods: $m=ncdot t$

Interest: $I=A-P$

Using this variables, the formula becomes,

$A=P(1+i)^m$

$$

I=A-P=P[(1+i)^m-1]

$$

a.) We shall find the effective annual interest rate for a semi-annual compounding (n=2) with $r=6.3%$.

$A=Pleft(1+dfrac{r}{n}right)^{nt}$

$Pleft(1+iright)^{1}=Pleft(1+dfrac{0.063}{2}right)^{2}$

Divide both sides by $P$ and solve for $i$

$$

i=left(1+dfrac{0.063}{2}right)^{2}-1=0.064=6.4%

$$

$Pleft(1+iright)^{1}=Pleft(1+dfrac{0.042}{12}right)^{12}$

$$

i=left(1+dfrac{0.042}{12}right)^{12}-1=0.0428=4.28%

$$

$Pleft(1+iright)^{1}=Pleft(1+dfrac{0.032}{4}right)^{4}$

$$

i=left(1+dfrac{0.032}{4}right)^{4}-1=0.0324=3.24%

$$

b.) $4.28%$

c.) $3.24%$