All Solutions

Page 498: Check Your Understanding

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

Just substitute the given values to the formula above.

a.) A = 10,000 , $i=0.4$, $m=10$

$$

PV=dfrac{10;000}{(1.04)^{10}}=$6755.64

$$

$$

PV=dfrac{100;000}{(1.031)^{10}}=$73;690.81

$$

$$

PV=dfrac{23;000}{(1.013)^{60}}=$10;506.47

$$

$$

PV=dfrac{2500}{(1.0055)^{1200}}=$3.46

$$

b.) $$73;690.81$

c.) $$10;506.47$

d.) $$3.46$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall calculate the present value of Kevin’s and Lui’s investment and compare them. Since the future value is the same, the one that requires more present value (initial investment) means the rate of growth is slower than the other, and thus would need to invest more to reach the goal at the same time.

Kevin: $P=10;000$, $i=0.05$, $m=20$ $implies PV=dfrac{10;000}{(1.05)^{20}}=$37;768.89$

Lui: $P=10;000$, $i=0.004$, $m=240$ $implies PV=dfrac{10;000}{(1.004)^{240}}=$3836.27$

Therefore, $boxed{bold{Lui; has; to; invest; more; than; Kevin}}$ to achieve the same goal.

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall calculate the interest $I$.

Remember that $A=PV+Iimplies I=A-PV$

a.) $P=10;000$ , $i=0.06$, $m=4$

$PV=dfrac{A}{(1+i)^m}=dfrac{10;000}{(1+0.06)^4}=$7920.94$

$$

I=10;000-7920.94=$2079.06

$$

$PV=dfrac{A}{(1+i)^m}=dfrac{6200}{(1+0.041)^6}=$4,871.78$

$$

I=6200-4871.78=$1328.22

$$

$PV=dfrac{A}{(1+i)^m}=dfrac{20,000}{(1+0.014)^{60}}=$8,684.66$

$$

I=20,000-8,685.66=$11;315.34

$$

$PV=dfrac{A}{(1+i)^m}=dfrac{12,800}{(1+0.0035)^{108}}=$8,776.74$

$$

I=12,800-8,776.74=$4023.26

$$

b.) $$1,328.22$

c.) $$11,315.34$

d.) $$4023.26$

$$

PV=8500

$$

$PV=dfrac{A}{(1+i)^n}$

Where $A$ is the future value. Since interest is compounded annually $i=0.072$

$8500

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We are given with $A=1429.50$, $r=18%=0.18$ , n = 12 (monthly compounding), $t=2$ years

Using the formula

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{ncdot t}}=dfrac{1429.50}{left(1+dfrac{0.18}{12}right)^{12( 2)}}=$1,000$

The total cost of the TV is the present value plus the $$900$ that he saved, which means,

$1000+900=$1900$

The original cost of the TV is $boxed{bold{$1,900.00}}$

$1,900

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We are given with $A=15000$, $r=10%=0.10$ , n = 4 (quarterly compounding), $t=10$ years

Using the formula

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{ncdot t}}=dfrac{15000}{left(1+dfrac{0.10}{4}right)^{4(10)}}=$5586.46$

The present value is $boxed{bold{$5586.46}}$

$5586.46

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

Colin did started with an initial investment followed by 3 additional 5000 at different intervals. We shall calculate the present value of the $5000$ added on the third interval.

Third interval: $A=5000$, $i=r/n=0.0179$ , $m=ncdot t=20$

$PV_3=dfrac{A}{(1+i)^m}=dfrac{5000}{(1+0.0179)^{20}}=$3506.45$

Second interval: $P=3506.45+5000=8506.45$ , $i=0.0179$, $m=8$

$PV_2=dfrac{8506.45}{(1.0179)^8}=$7380.87.67$

First interval: $7380.87+5000=12380.87$ , $i=0.0179$ , $m=12$

$PV_1=dfrac{12380.87}{(1.0179)^{12}}=10,006.67$

Therefore, the initial investment was $boxed{bold{$10,006.67}}$

$10,006.67

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We are given with

$A=6000$

$PV=2500$

$n=4$ (compounded quarterly)

$t=10$ years

Substituting these to the formula

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{ncdot t}}$

$2500=dfrac{6000}{left(1+dfrac{r}{4}right)^{4(10)}}$

$(1+0.25r)^{40}=dfrac{6000}{2500}$

$1+0.25r=left(dfrac{6000}{2500}right)^{1/40}$

$1+0.25r=1.022128$

$r=dfrac{1.022128-1}{0.25}=0.0885=8.85%$

The annual interest rate is $boxed{bf{8.85%}}$

8.85%

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall calculate the initial investment of Franco

$A=25000$ , $i=r/n=0.069$ , $m=ncdot t=30$

$PV_{F}=dfrac{A}{(1+i)^m}=dfrac{25,000}{(1+0.069)^{30}}=$3377.60$

For David,

$A=25000$, $i=r/n=0.00575$ , $m=ncdot t=360$

$PV_D=dfrac{25,000}{(1.00575)^{360}}=$3173.40$

Since $PV_F>PV_D$, $boxed{bf{Franco; invested; more; than; David}}$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall calculate the present value for the second interval when $A=14;784.56$, $i=0.018$ and $m=24$

$PV_2=dfrac{14;784.56}{(1+0.018)^{24}}=$9635.22$

The present value on the first interval can be obtained by setting $PV_2$ as the new $A$ with $i=0.06$, $m=5$

$PV_1=dfrac{9635.22}{(1+0.06)^5}=$7200$

Therefore, Sally’s first investment was $boxed{bold{$7,200}}$

$7,200

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

a.) Steve has two options, the 5-year guarantee and the 8-year guarantee. To determine which one is more profitable, we shall calculate the present value for the same final value of $$25,000$. The investment plan that requires lower initial investment is better.

For the 5-year guarantee

Second interval: $A=25,000$ , $i=0.01$ , $m=80$

$PV_2=dfrac{A}{(1+i)^{m}}=dfrac{11,277.95}{(1+0.01)^{80}}=$11;277.95$

First interval: $A=PV_2=11,277.85$ , $i=0.008$ , $m=20$

$PV_1=dfrac{11,277.85}{(1+0.008)^{20}}=$9,616.56$

For the 8-year guarantee

Second interval: $A=25,000$ , $i=0.0125$ , $m=68$

$PV_2=dfrac{25000}{(1+0.0125)^{68}}=$10;741.82$

First interval: $A=PV_2=10,741.82$, $i=0.008$ , $m=32$

$PV_1=dfrac{10;741.82}{(1+0.008)^{32}}=$8324.17$

Steve must choose the 8-year guarantee since it requires lesser initial investment.

b.) $$8,324.17$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall examine the similarity between the equations for present value of compound interest and the equation for the disintegration of radioactive material. As mentioned above, the present value of compound interest is

$PV=dfrac{A}{(1+i)^m}=A(1+i)^{-m}$

while the amount of radioactive material $A$ decreases from its initial amount $A_0$ as

$A=A_0cdot exp(-kt)$.

Observe that both functions are decreasing and exponential with respect to time (the time is at the exponent).

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

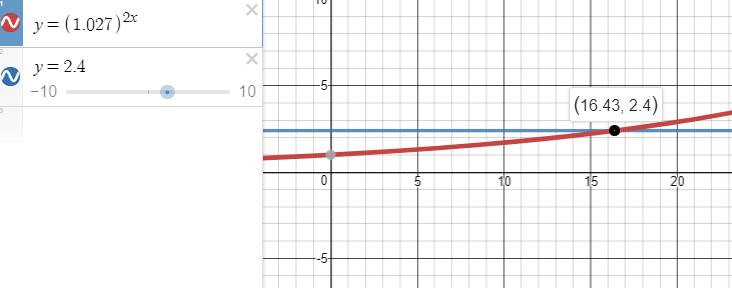

We shall find how long it takes for an initial investment of $PV=5000$ to reach $A=12000$ at $i=0.0272$ for semi-annual compounding $n=2$.

$PV=dfrac{A}{(1+I)^{nt}}implies 5000=dfrac{12000}{(1+0.0272)^{2t}}$

$5000(1.027)^{2t}=12000$

$(1.027)^{2t}=2.4$

$(1.027)^{2t}=2.4$

$(2t)(log 1.027)=log(2.4)implies t=dfrac{log(2.4)}{2log (1.027)}approx 16.4303$

But don’t worry if this doesn’t make sense to you right now.

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

We shall find the annual interest rate so that the initial investment would be triple its value after $10$ years for quarterly compounding.

This means $A=3PV$ at $n=4$, $t=10$

Using the equation above,

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}$

$PV=dfrac{3PV}{left(1+dfrac{r}{4}right)^{4(10)}}$

PV can be cancelled out

$(1+0.25r)^{40}=3$

$1+0.25r=3^{1/40}$

$1+0.25r=1.027846$

$r=dfrac{1.027846-1}{0.25}$

$r=0.1114=boxed{bf{11.14%}}$

Therefore, an annual interest rate of $11.14%$ is needed to triple an investment in 10 years.

11.14%

$$

The present value PV of an investment or debt in a compound interest is

$PV=dfrac{A}{left(1+dfrac{r}{n}right)^{nt}}=dfrac{A}{(1+i)^m}$

$A$ = future value after $t$ years

$r$ = annual interest rate

$n$ = number of compounding per year (annually = 1, semi-annually = 2, quarterly = 4, monthly = 12)

$t$ = number of years

$m$= total number of compounding after $t$ years = $ntimes t$

$i$ = interest rate per compounding = $r/n$

Equal payments of $268.17$ was done 30 times so the the total amount paid is

$A=30(268.17)=$8045.10$

To know the original amount borrowed, we shall calculate PV with $i=0.016$ and $m=30$

$PV=dfrac{A}{(1+i)^{m}}=dfrac{8045.1}{1.016^{30}}=boxed{bf{$4997.12}}$

The interest paid is

$I=A-PV=8045.10-4997.12=boxed{bf{$3047.98}}$

Therefore, he borrowed $$4997.12$ and paid an interest of $$3047.98$.

$A=PV(1+rt)$

So the formula for present value can be written as

$PV=dfrac{A}{1+rt}$

PV=dfrac{A}{1+rt}

$$